In its latest quarterly report on Iran’s economic performance, the Middle East Bank reviewed fluctuations in the country’s foreign exchange market in the last Iranian year (ended March 20, 2017).

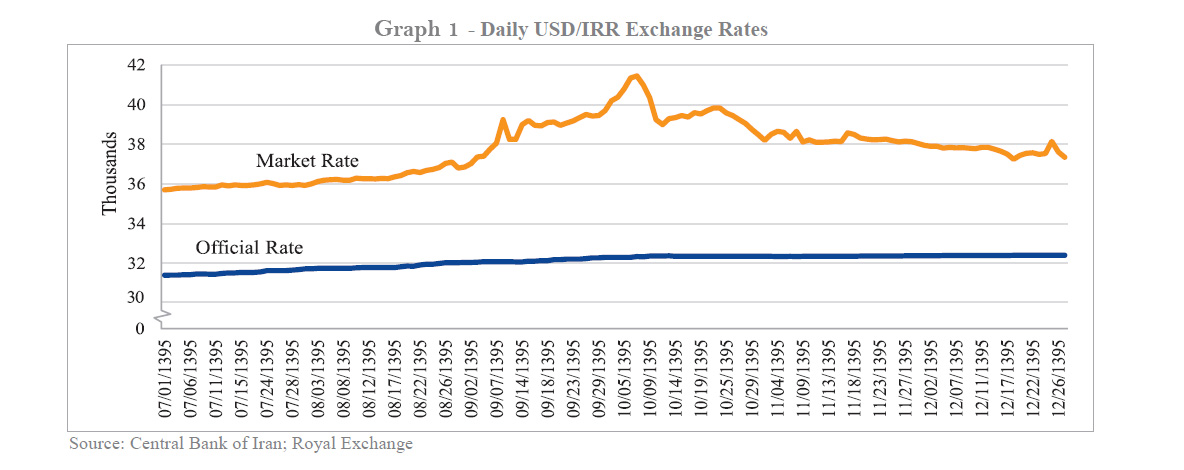

According to the report, the US dollar/rial market exchange rate, which surpassed 39,000 rials in Q3 of the last Iranian year, surged to 41,450 rials in the first week of Q4 to mark the maximum nominal exchange rate of the dollar since President Hassan Rouhani took office in Aug. 2013.

The drop in the supply of foreign exchange as a result of petrochemical companies’ reluctance to exchange their export proceeds in the hope of benefiting from the surge in this exchange rate, coupled with rising demand by commercial companies for their international transactions, exerted upward pressure on the exchange rate in Q3 of the last Iranian year and the first week of Q4.

Expectations of the dollar further strengthening against rial also had its share. The Central Bank of Iran’s intervention brought this rate down to below 40,000 in the second week of Q4.

In the final month of the last Iranian year, this rate dipped below 38,000 rials and fluctuated around 37,700. Graph 1 exhibits the daily market and official exchange rates in the second half of the last Iranian year.

As observed in Graph 1, in contrast with the market exchange rate, its official rate did not experience much change in the second half of last year and on average increased by less than 1% a month during the last five months of the year.

These developments have widened the gap between the official and market exchange rates from 14% at the beginning of fall to 16.4% at the end of winter, making it more difficult for CBI to proceed with its long-overdue exchange rate unification.

Graph 2 depicts the average annual inflation rate and the average growth rates of official and market exchange rates in 12-month periods culminating in the last day of each month in the past two years.

As can be seen in Graph 2, the domestic annual inflation rate increased to 9% in the final month of the last Iranian year after remaining at 8.6% for three months. The inflation rate is expected to rise further in the current Iranian year and this would raise the exchange rate if CBI does not intervene in the market.

Apart from the domestic inflation rate and CBI’s policies, uncertainties related to the new US administration’s policy toward Iran and the nuclear deal are among factors affecting exchange rate developments.

CBI planned to change the currency in reporting foreign trade statistics from dollar to other foreign currencies at the end of the last Iranian year.

Since Iran’s international trade is mainly with European countries and China, the dollar accounts for a small proportion of Iran’s international transactions. As the dollar’s exchange rate against other major currencies has been volatile in recent months, reporting all foreign revenues in terms of dollar will result in imprecise figures in income statements.

From CBI’s point of view, it is more preferable to report foreign revenues in terms of a currency with low volatility. On the other hand, CBI likes to lighten the dominant role of dollar in the formation of domestic inflation expectations.

The change in reporting currency can be implemented by either selecting “the foreign currency with the highest share in international trade” or a “basket of currencies”.

According to CBI authorities, the change in reporting currency will reduce fluctuations in foreign exchange market.

But this expectation may not be realistic, as changing the reporting currency is an accounting issue that will only result in nominal changes rather than real ones.