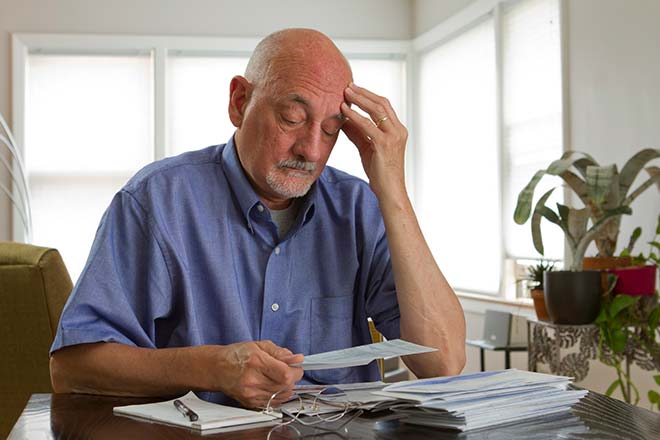

A growing number of retirees in the US are filing for bankruptcy in an attempt to halt some of their monthly payments as pensions have largely declined, savings have shrunk and bills have piled up.

A recent study conducted by four professors citing data from the Consumer Bankruptcy Project demonstrated an alarming trend among seniors who are 65 to 74 years old–the number of seniors filing for bankruptcy jumped from 1.2 per 1,000 in February 2013 to 3.6% per 1,000 in November 2016, US News reported.

The bankruptcy rate for Americans at least 75 years old more than tripled from 1991 to 2016, while filings among those between 65 and 74 ballooned more than 200%, according to the study.

After decades of cutbacks in salaries and jobs, fewer pensions that were funded by employers, rising health care costs and supporting adult children, more retirees are now facing this new dilemma as life expectancy rates continue to rise and more people live past 80.

Lacking any other options, some retirees who receive inadequate income from jobs and meager savings from their 401(k) plans are surviving by heading to bankruptcy court.

“The magnitude of growth in older Americans in bankruptcy is so large that the broader trend of an aging US population can explain only a small portion of the effect,” wrote professors Deborah Thorne of the University of Idaho, Pamela Foohey of the Indiana University Maurer School of Law, Robert Lawless of the University of Illinois College of Law and Katherine Porter of the University of California-Irvine School of Law in their research paper.

Increase in Financial Burden

The increase in financial burden means that the retirees are filing for bankruptcy with a median negative wealth of $17,390 compared to more than $250,000 for their peers who are not filing.

“For an increasing number of older Americans, their golden years are fraught with economic risks, the result of which is often bankruptcy,” the authors wrote.

Whether or not they’ve assembled an impressive investment portfolio, people who are getting close to retirement can avoid having to file for bankruptcy by paying off debt and giving priority to credit cards with the highest interest rates, says Ron McCoy, CEO of Freedom Capital Advisors in Winter Garden, Florida.

Establishing an aggressive plan to eliminate debt is crucial, says Bruce McClary, spokesman for National Foundation for Credit Counseling, a non-profit organization. After paying off credit card debt, baby boomers should target their mortgage and auto loans.

“The less debt you carry into retirement the more you will have to cover the necessities like food and health care,” he says. “Getting help with this plan is as easy as reaching out to a nonprofit credit counseling agency or talking with your financial advisor.”

Tackling Debt

There are several strategies to tackling credit card debt and managing your home loans.

“It is just a matter of selecting the method that makes the most sense for you,” McClary says. “You can weigh the benefits of refinancing, selling or getting a reverse mortgage.”

Parents should also ensure they communicate with their children on whether they will help finance a down payment for a house or cosign for an auto loan since many people are spending a couple of decades in retirement and will need additional income.

“People need to let their children know now that they are not going to be able to help out financially so that when the kids come asking, they have already been told what to expect,” McCoy says.

Accruing more debt is a trap that many seniors fall into because they believe it will help their child or another relative.

“This means no cosigning loans for family members, student loans, home equity loans for vacations or retail purchases and signature loans for vacations,” says McClary. “Simply put, it’s time to stop piling on debt and start chipping away at what you already owe.”

Downsizing is another approach which is beneficial for many people as they get closer to retiring. Their options include buying or renting a smaller home, selling an extra vehicle and making a plan for the “inevitable reduction of income that will require a leaner budget,” McClary says. “Getting a head start on those lifestyle changes will help make the transition to retirement a more affordable and enjoyable experience.”

“The most significant concern most people have about retirement is running out of money,” he says.

Retirees need about 80% of their pre-retirement income to maintain their desired standard of living in retirement–someone earning $60,000 would need $48,000 annually. People who generated average wage earnings should expect their Social Security benefits to mirror the same.

“Social Security benefits may only replace 40% of your needs,” Ulin says. “Depending solely on Social Security to pay your bills in retirement may not work out for in the long run, especially if you are still carrying a mortgage, car loan and other obligations.”

Expenses in retirement can be more than many people estimate since the cost of living may increase by 50% every decade based on a 3.4% inflation rate, he says.

“Individuals don’t take enough risk and put assets into money market funds when they are decades away from retirement,” says Robert Johnson, principal at the Fed Policy Investment Research Group in Charlottesville, Virginia.

Retirees who can delay taking Social Security payments should choose this option. Many people take Social Security as soon as they are eligible.