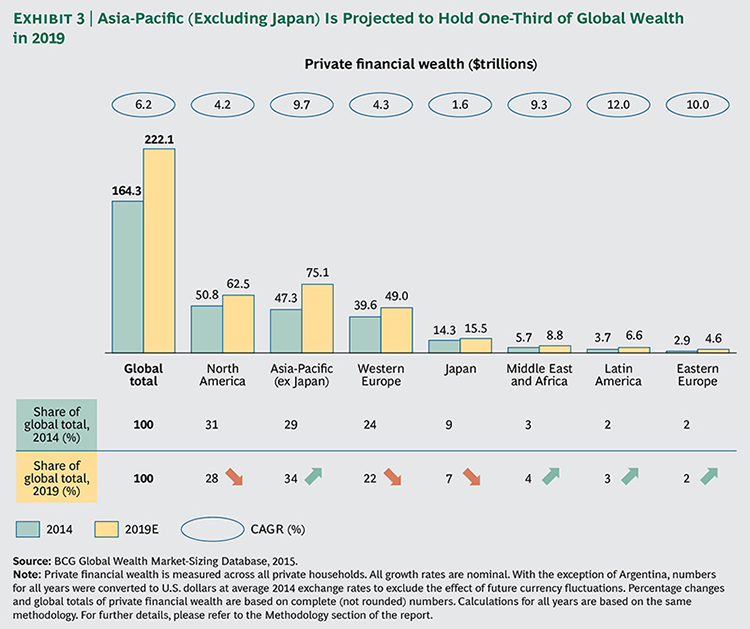

Private financial wealth in the Asia-Pacific region (excluding Japan) overtook Europe's last year as China minted a million new millionaires, according to a study by The Boston Consulting Group.

Asia Pacific (ex-Japan) is projected to have $57 trillion in private financial wealth in 2016, surpassing North America's $56 trillion, Bloomberg reported.

A strong “old world versus new world” dynamic is driving the wealth shift, the BCG study found. Asia-Pacific (ex Japan) recorded the fastest growth in wealth in 2014, with an expansion of 29%.

Millionaire households held 41% of global private wealth last year, up from 40% a year earlier. They're projected to hold 46% of global private wealth in 2019.

The US still had the most number of millionaire households in 2014 (7 million), followed by China (4 million), and Japan (1 million). When it comes to the density of millionaires, Switzerland came out top with 135 out of every 1,000 households having private wealth greater than $1 million. Bahrain (123), Qatar (116), Singapore (107), Kuwait (99), and Hong Kong (94), rounded out that list, showing when it comes to wealth, smaller is better.

For Europe's private bankers, the report has a warning: "Switzerland will need to reinvent itself to resist the threat from fast-developing Asian booking centers as preferred locations for offshore wealth,'' it said. Hong Kong and Singapore accounted for 16% of global offshore assets in 2014 and are expected to grow in prominence.

A caveat -- Chinese and Indian investments in local equities drove much of the wealth gain for Asia last year. And as they say, what goes up…

China's $1 Trillion Province

China unveiled free-trade zones in three provinces recently as it pushes ahead with opening up more areas of its economy.

An FTZ in Guangdong will fuse the province's economy more closely with Macau's and Hong Kong's and boost yuan-denominated trade and financing. Guangdong, Hong Kong and Macau's combined output exceeded that of Mexico, South Korea and Spain in 2014, according to IMF estimates and data compiled by Bloomberg.

The population of 107 million in Guangdong–a production hub for electronics, garments and automobiles–exceeds that of Germany's and Vietnam's.

The other two FTZs that kicked off in April after a trial period were in neighboring Fujian province and the municipality of Tianjin, less than an hour from Beijing by the high-speed train.

Tianjin, with about 15 million people, had output of $253 billion last year, more than Pakistan, Portugal and Peru. Fujian's output of $387.5 billion last year was about equal to the economies of Thailand or South Africa.

It's all part of Premier Li Keqiang and President Xi Jinping's push for a more market-driven economy with fewer financial restrictions and more innovation. The FTZs echo the approach former supreme leader Deng Xiaoping took when opening the economy to trade and investment in the 1980s through special economic zones such as Shenzhen.

"Deng's special economic zones opened China's trade in 1980s–now the free-trade zones aim at opening China's capital market,'' said Li Xiaoyang, assistant professor of economics and finance at Cheung Kong Graduate School of Business in Beijing. "Now we often talk about the dividend of reform, and that dividend will come next from the opening of the capital market.''

The Guangdong zone is limited to three districts in the province and has several exceptions to the "free-trade'' designation. It's aimed at boosting manufacturing and financial services.

It "will be a window to Hong Kong, Macau and Southeast Asia,'' said Zhou Hao, an economist at Australia & New Zealand Banking Group in Shanghai. An aim of the FTZ is "to help upgrade the traditional trade sector and move up the value chain.''