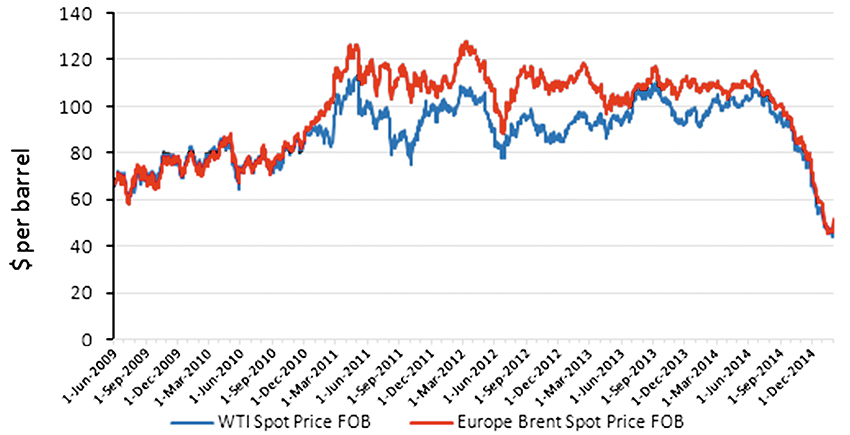

The price of oil has more than halved in less than 11 months since September 2014.

After nearly five years of stability, the price of a barrel of Brent crude in Europe fell from over $100 on September 2014 to less than $49 on August 2015.

There are several reasons for this rapid drop, including supply and demand conditions and oil market expectations.

Part of the recent price collapse can be attributed to the glut in oil supply. Unconventional energy resources, such as shale oil, shale gas and oil sands, have raised the global oil supply. Massive discoveries of oil in North Dakota and Texas have driven down prices, even amid tensions in the Middle East and Ukraine, and roughly 3 million more barrels a day are being produced now than in 2011.

In addition, while oil prices were falling, the Organization of Petroleum Exporting Countries, which controls nearly 40% of the world market, failed to reach an agreement on production curbs at two meetings in Vienna on 27 November 2014 and on 5 June 2015, thus sending the price down even further.

Two main reasons have been cited for the reduction in oil demand. The first reason is that demand for energy is closely related to economic activity, such that weaker economic activity resulted in a fall in demand for oil. The second reason is not related to economic activity but to monetary policy.

Weaker Economic Activity

The International Monetary Fund has downgraded its forecast for global economic growth for 2015 by 0.3% to 3.5%. The downgrade comes despite the economic boost provided by lower commodity prices.

The IMF has cited weaker investment outside the United States and growth fears in emerging markets such as the Russian Federation, the People’s Republic of China and Brazil as the primary reasons for the downgrade in growth. This has reduced oil demand in certain areas and resulted in weak growth for global oil demand, which has had a negative impact on oil prices.

Weaker global oil demand growth has contributed to rising global oil inventories. In January, the Organization for Economic Cooperation and Development estimated that total commercial oil inventories had reached their highest levels since August 2010.

Global oil demand dropped toward the end of 2014. A part of this drop in demand is due to the aforementioned reasons. However, this is not the whole story.

Monetary Policy

Before discussing how monetary policy was behind the oil price drop, let’s look further back to the subprime mortgage crisis of 2008–09 and review what happened to the US money market and global oil prices at that time.

After the subprime mortgage crisis, the weak exchange rate of the US dollar, caused by the country’s quantitative easing, pushed oil prices in US dollars upward over the period 2009–12 by causing investors to invest in the oil market and other commodity markets while the world economy was in recession. As a result, huge amounts of capital entered the crude oil market as investors found it safer than capital markets, which had collapsed.

Because of this new demand, oil prices started to rise sharply in 2009, when the US and many other economies were in recession. This trend had the effect of imposing a longer recovery time on the global economy, as oil has been shown to be one of the most important production inputs.

Now, let’s move to the end of 2014 to see what has happened more recently. In 2014, financial conditions eased compared to 2013. In particular, long-term interest rates declined in advanced economies because of the economic recovery and expectations of a lower neutral policy rate in the US over the medium term.

Equity prices have generally risen and risk premiums declined in advanced economies and emerging markets. In the US, both the Dow Jones Industrial Average and the S&P 500 powered to record highs, boosted by the strengthening US economy and liquidity provided by the Federal Reserve’s unprecedented quantitative easing.

The Dow, up 8.5%, surpassed two key psychological levels during the year 2014—17,000 and 18,000. And the S&P 500, 12.8% higher, also surpassed the 2,000 milestone.

This means that the liquidity mainly provided by the Federal Reserve, especially during the 2008–09 financial crisis, moved into the oil market and created a huge demand and a surge in oil prices.

Now, because the US and some other advanced and emerging capital markets are recovering, it has moved back to the capital markets. This is the reason for the reduced global oil demand, which resulted in the price collapse. This means that this factor may have played a stronger role than supply and lower economic growth.

- Naoyuki Yoshino, Ph.D.

Dean, Asian Development Bank Institute (ADBI)

Professor Emeritus Keio University, Tokyo, Japan

- Farhad Taghizadeh-Hesary, Ph.D.

Assistant Professor of Economics, Keio University, Tokyo, Japan

Research Assistant to Dean, Asian Development Bank Institute (ADBI)