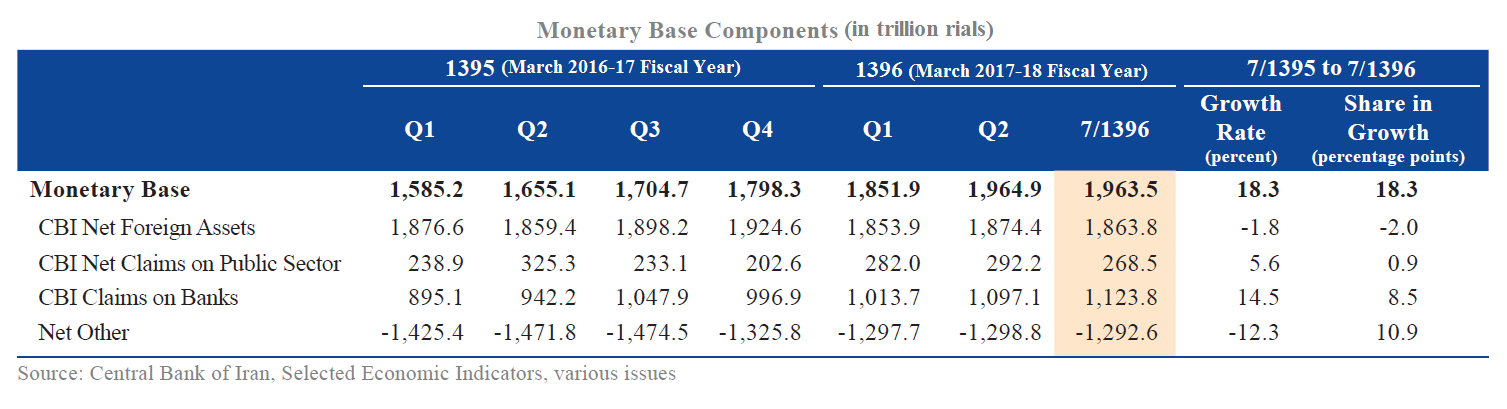

At the end of the current fiscal year’s seventh month (Sept. 23-Oct. 22), the balance of monetary base rose by 18.3% from a year earlier and by 9.2% from the year’s beginning.

The 12.3% fall in “net other” category, as a factor of decrease in monetary base, constitutes the main factor behind the rise in monetary base. The 14.5% rise in the Central Bank of Iran’s claims on banks due to the rise in CBI’s claims on non-public banks and non-bank credit institutions was the second factor triggering the growth.

During the period under review, CBI claims on non-public banks and non-bank credit institutions rose by 135.8% despite a 37.4% fall in CBI claims on commercial banks and 16.3% fall in that of the specialized banks.

Accordingly, the share of non-public banks and non-bank credit institutions in CBI’s claims on banks rose to 46.9% during the month under review from 22.8% in last year’s corresponding month. This 46.9% growth indicates that the banking system was short of funds to cover interest payments and loan extensions and thus CBI, as the lender of last resort, has had to fill the shortage.

The 5.6% rise in CBI’s net claims on public sector, which was the result of the rise in CBI’s claims on government and the fall in government deposits with the CBI, constitutes the third factor in that monetary base expansion, reads the Middle East Bank’s latest quarterly report.

CBI’s claims on state-owned companies and institutions have fallen while their deposits with the CBI have risen. Even though the share of these companies and institutions in total CBI claims on public sector has fallen, it is still as high as 72.3%.

The 1.8% fall in net foreign assets of CBI during the period under review was a contractionary factor in monetary base, indicating that foreign debts have grown faster than foreign reserves.

M2 money multiplier rose by 10 basis points from 7 to 7.1 at the end of the seventh month. The fall in the ratio of notes and coins with the public to total deposits, coupled with the fall in the ratio of banks’ excess reserves to total deposits were behind the increase in M2 money multiplier, while the rise in the ratio of banks’ legal reserves to total deposits was a factor of decrease.

As a result of the simultaneous rise in monetary base and M2 money multiplier during the period under review, M2 liquidity rose by 23.3% to 14,030.5 trillion rials ($307 trillion) at the end of the month. This jump was less than its 28.3% growth in the preceding year’s similar month due to the slower rise in M2 money multiplier.

M1 money rose by 13% and quasi-money by 24.8%, accounting for 1.7 and 21.6 percentage points of M2 liquidity growth, respectively. Among M1 money components, notes and coins with the public rose by 5.2% and sight deposits by 15.2%, accounting for 0.2 and 1.5 percentage points of M2 liquidity growth, respectively. Accordingly, M1 money accounted for 11.7% and quasi-money for 88.3% of the M2 liquidity.

Balance of deposits, deposits after deduction of legal reserves and extended facilities of the banking system at the end of the seventh month show a 21.6%, 21% and 19.2% growths, respectively. The ratio of the balance of extended facilities to deposits (after the deduction of legal reserves) fell by 1.3 percentage points to 84.0%. The upward trend of this ratio in Q4 of last year reversed course in Q1 this year and remained at 84%.

Point-to-point growth of balance of deposits and deposits after deduction of legal reserves, which had started to increase from the beginning of the year, reversed course and followed a downward trend in the aftermath of CBI’s imposition of a cap on deposit interest rates.

It should be noted that the ratio of legal reserves to total deposits of the banking system rose by 0.4 percentage points to 10.1% at the end of the month.

The latest CBI statistics indicate that during the first eight months of the year, approximately 3,574.3 trillion rials ($78.4 billion) of facilities have been extended, indicating a 9.6% rise.

The share of various sectors in the extended facilities was 7.3% in agriculture, 29.8% in industries and mining, 8.5% in housing and construction, 14.2% in commerce and 40.1% in services. Of the total facilities, 62.5% were aimed at financing working capital, 2.8 percentage points below that in its preceding year.

Financing working capital accounted for 84.4%, 50.9% and 71.1% of the facilities extended to industries and mining, services and commercial sectors, respectively.