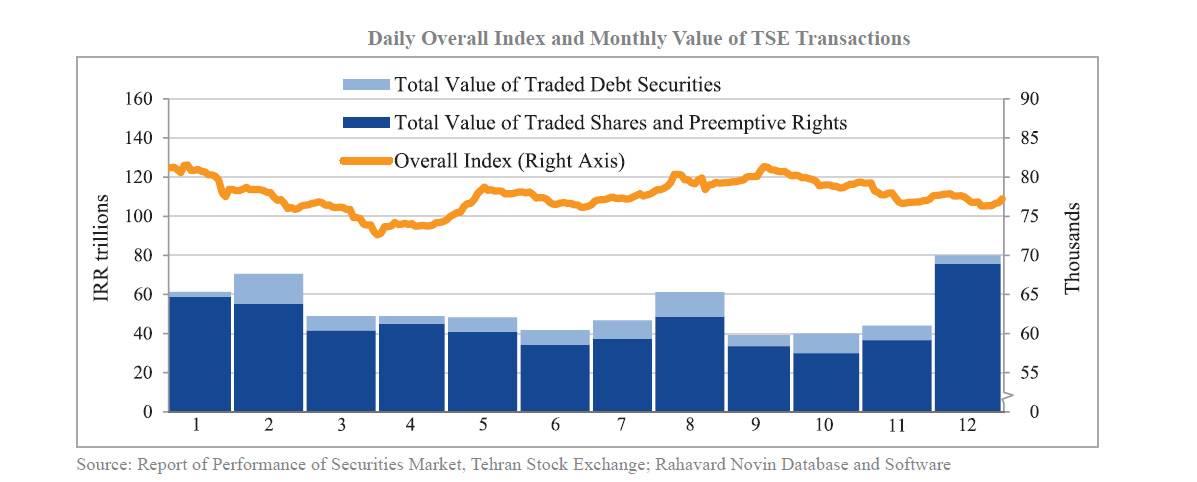

The overall index of Tehran Stock Exchange closed at 77,230 at the end of the last Iranian year (ended March 20, 2017), showing a 2,900-point drop from the last day of fall (Dec. 20, 2016).

As shown in the following graph, after surpassing 80,000 at the end of fall, the overall index dropped from the beginning of winter and fluctuated between 76,000 and 79,000 in the last two months of the year. The value of transactions at TSE was higher in winter than in fall and peaked in the last month of winter. However, the value of traded debt securities dropped in winter.

The value of transactions in “shares and preemptive rights” and “debt securities” were 75.7 trillion and 4.3 trillion rials in the last month of winter (ended March 20, 2017), respectively, according to the Middle East Bank’s review of Iran’s capital market performance in its latest quarterly report.

The sixth series of Islamic Treasury Bills matured in Q3 of the fiscal March 2016-17 and the principals were fully paid on time. All series of these bills are published by the Ministry of Economic Affairs and Finance with a one-year maturity.

Normally, it takes about four months for these bills to become tradable in the stock market. The seventh to 10th series of the bills became tradable in Q2 and Q3 of 1395, and the 11th series valued at 15 trillion rials ($400 million) became tradable in winter.

As these securities are essentially risk-free and have higher rates of return than other low-risk investment alternatives, they are more attractive than stocks. This prompted some analysts to blame the low stock returns in the second half of the last Iranian year to the issuance of a high volume of Islamic Treasury Bills.

In response to this criticism, the scheduled issuance of new series of Islamic Treasury Bills did not take place by March 2017.

Although at the end of the year the value share of Islamic Treasury Bills in the market was only 1.8%, its share of the free float stocks ranged between 15% and 20%. Hence, the claim that such securities affect the demand for other securities is not unfounded.

However, the roots of the low stock return are elsewhere and it may not be wise to forego the benefits of the debt market in the hope of achieving higher returns in the stock market.