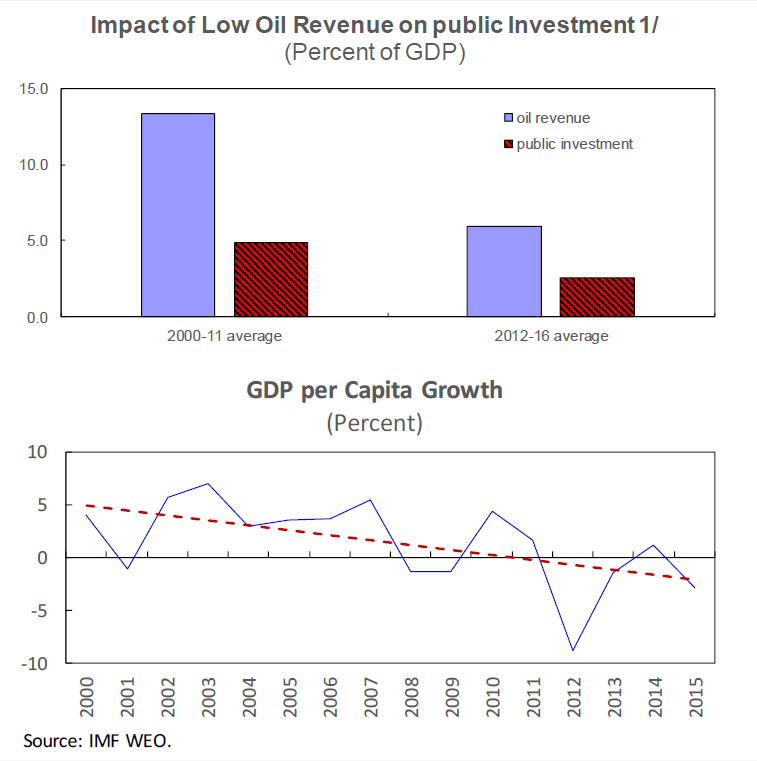

Since the early 2000s, growth in Iran has been insufficient to improve real GDP per capita incomes.

Sanctions and negative oil price shocks led to budget tightening and a contraction in pro-growth spending. Investment in infrastructure has been cut in half since 2012 (Figure 1).

Looking ahead, lower public investment could constrain Iran’s growth potential. On the other hand, it is possible that an increase in government revenue would be followed by an aggressive scaling up of public investment.

A working paper recently published by International monetary Fund has analyzed how Iran could increase its public investment to achieve higher growth while preserving a fiscally sustainable path that avoids explosive and unsustainable debt or excessively tight tax policies that would be impossible for the government to maintain in the long run.

Fundamentally, a relaxation of the fiscal stance to finance a large temporary increase in investment faces two hurdles.

First, scaling up too abruptly leads to inefficiencies. For example, selected projects may be of lower quality, making the entire process more inefficient.

Second, increasing investment requires building fiscal buffers, so that in case of adverse shocks, such as an unexpected decrease in oil revenue, the investment plan could still be carried out without compromising fiscal stability.

Furthermore, scaling up investment may shift financial resources from the private to public sector and have a distortionary effect by increasing interest rates and crowding out private investment.

Investment, Oil Price Scenarios

The paper has defined and examined multiple scenarios for investment scaling-up: (1) A “gradual” scenario, in which investment would increase by 3% of GDP over four years and would then remain stable at its 10-year, pre-sanctions (2002-11) average of 5.2% of GDP; (2) A “conservative” scenario, in which the same amount of increase in public investment takes place over eight years, instead of four, before it reaches the same long-run level as in the gradual scenario; and (3) An “aggressive” scenario that, in three years, leads to the highest level of public investment in Iran in two decades, before stabilizing at the long-run level of 5.2% of GDP.

It also defined two oil price scenarios: In the “baseline” scenario, oil prices are assumed to reach $55 a barrel by 2021, while under the “adverse scenario,” oil prices never exceed $48 a barrel.

Finally, investment is examined in an “efficient” scenario, where it is assumed that the share of nominal investment that turns into productive capital is larger, allowing us to study the growth impact of structural reforms that improve public investment efficiency when oil prices are low.

The “oil fund” scenario is also surveyed, in which the government can deplete the National Development Fund of Iran completely. It enables us to analyze the impact of such a mechanism when oil prices are low.

While the analysis shows that scaling up investment is viable under all scenarios, since gross debt remains on a declining path in the long run and accumulating wealth continues, the costs of an aggressive strategy are considerable.

An aggressive frontloading of public investment results in 0.9 percentage points of higher growth, relative to the growth that can be achieved under the gradual scenario. However, that comes at the cost of a 1 pp higher consumption tax rate than what would be needed with the gradual approach (2 pp in the adverse scenario) and 4 pp higher accumulation rate of public debt in the short run (10 pp in the adverse scenario). Furthermore, there will be a larger appreciation in the real exchange rate under the aggressive public investment scenario, eroding the competitiveness of the tradables sector.

The costs are higher when aggressive public investment coincides with a period of low oil prices (adverse scenario). However, the government is better off with an aggressive investment approach when the oil price is persistently low, if it can improve the efficiency of public investment.

Alternatively, when public investment is twice as efficient as in the baseline, the margin of growth, due to expansion in public investment, is larger: 2.1 pp versus 1.0 pp in the adverse scenario. Rising efficiency does not help with the size of fiscal adjustment that is required to close the fiscal gap.

Furthermore, the government can also use the oil fund to decrease the size of the adjustment needed to finance the scaling up of capital expenditures.

If full depletion of the oil fund is allowed, the increase in the consumption tax rate, which is needed to close the fiscal gap, will be less than 0.3 pp (compared to 2 pp in the adverse scenario), and gross debt will increase by only 1 pp (compared to 10 pp in the adverse scenario) because the government fully utilizes its financial assets.

The depletion of the oil fund, however, comes with other costs, such as large appreciation of the real exchange rate and current account deficit. It will also make the economy more vulnerable to exogenous oil price shocks and compromises macroeconomic stability in the medium and long run.

An oil fund is necessary to smooth government consumption and without one, the swings in government revenue will transfer the volatility in global oil prices to the economy, especially if access to international debt markets are limited.