Recent fluctuations in the rial/dollar exchange rate have prompted a lively debate among economists and financial experts in Iran over forecasting currency movements.

A lot of ink has been spilt in academic papers on the historic trends of the rial’s exchange rate carried out by domestic economic research institutes and international organizations such as the IMF.

The academic studies can be divided into two categories:

1. The Purchasing Power Parity Theory

This theory is based on calculating the flow of goods and services through the current accounts of two countries to determine the rate of exchange between their currencies.

Principally, the PPP theory implies that in a simple economy, demand for foreign currency stems from demand for imports while its supply derives from export revenues.

The most popular theory underpinning these assumptions is known as PPP that, despite or because of its longstanding history, remains as controversial as ever among economists.

According to the PPP theory, as an alternative to using market exchange rates, the relative value of two currencies is determined by the ratio of the price differences between a standard market basket of goods in those countries. Hence, exchange rate movements are determined by the rate of change between the inflation rates of two countries.

Empirical studies of exchange rates suggest that the time periods researched are critical in the concluding analysis of currency movements, as well as modifications applied to the data.

Academic and empirical studies of the rial/dollar exchange rate have ended up with different results and sometimes contradictory conclusions.

Some researchers, such as Oskooee (1993), Khataee and Khavarinejad (1996), and Bagheri (1997), have confirmed that the PPP theory is consistent with empirical data in Iran, whereas Zolnoor and Amiri (1996) and Dargahi (1997) suggested that the PPP theory is not consistent with parallel exchange rate behavior.

However, to this date, the theory holds valid for many economists. In a recent conference held by Tehran Chamber of Commerce, Industries, Mines and Agriculture, for example, some economic experts argued that the Central Bank of Iran should adjust the exchange rate by devaluing the rial by 6% against the dollar annually, assuming US inflation in dollar terms and Iranian inflation of 4% and 10% respectively.

2. Long-Term Behavior of Real Exchange Rates

Other academics took a different tack. Ebrahimi (1993), Yavari (1995), Pedram (1998), Ghasemlou (1998), and Sandarajan, Lazare and William (1999), and Dargahi (2001) developed empirical models to explain the behavior of real exchange rates through economic fundamentals.

To explain in brief: The production of goods is grouped into two categories, tradable and non-tradable goods. Typically, non-tradable goods include such items as electricity, water supply, all public services, hotel accommodation, real estate, construction, local transportation, goods with very high transportation costs such as gravel, and commodities produced to meet special customs or conditions of the country.

In oil exporting countries with growing oil revenues, the influence of tradable goods on the economy is very significant; hence it is vital to distinguish between these two types of goods in calculating their inflation in relation to other economies.

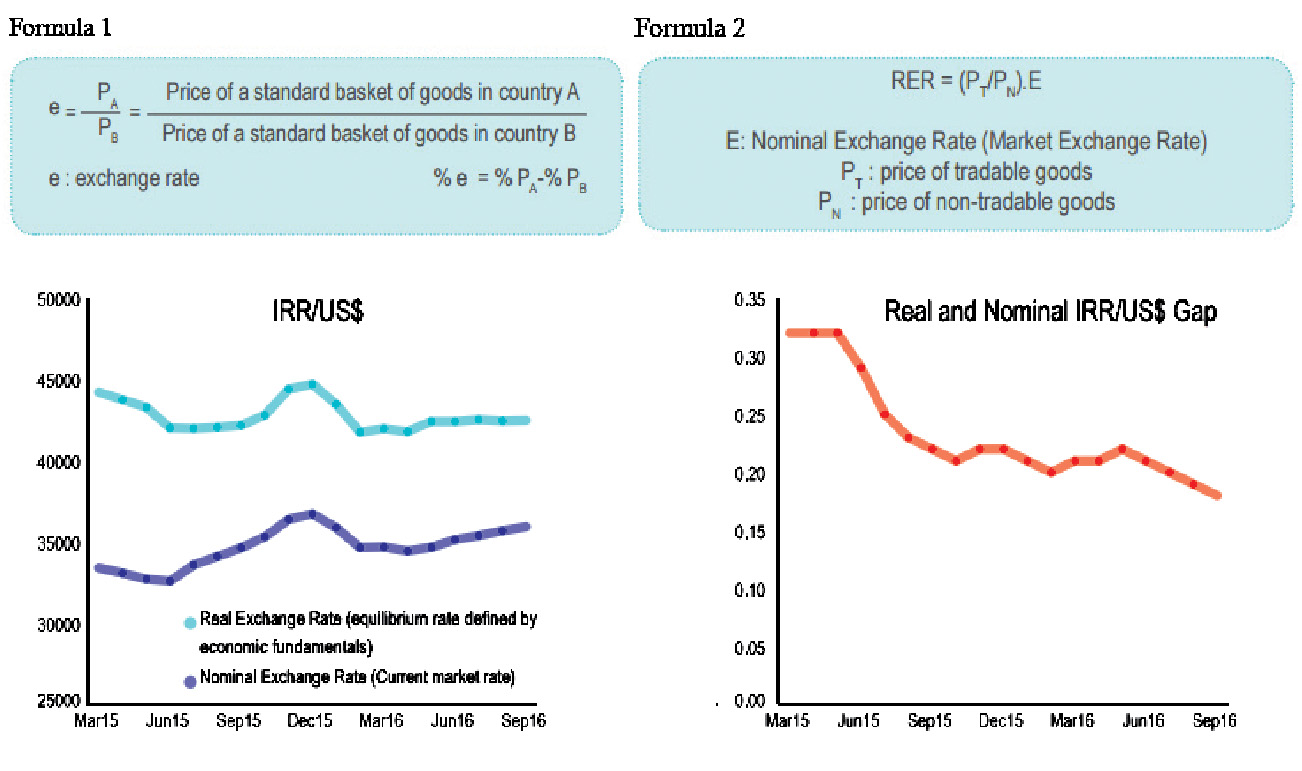

Therefore, the real exchange rate is estimated by an adjustment to the nominal exchange rate (market exchange rate), taking into account the price ratio of tradable and non-tradable goods.

Hence in the model set out by Dargahi (2001), the real exchange rate of the Iranian currency is examined against economic fundamental variables. The dependent variable model of the Real Exchange Rate of the IRR against the US dollar is calculated through formula 2.

Going further, Dargahi found a long-term relationship between fundamental variables and RER. This finding suggested that over the long term, RER behavior could be explained by macroeconomic indicators, namely government expenditure, investment and world oil prices.

The fundamental economic variables are listed as follows:

1- Total export revenue

2- Total factor productivity (TFP) growth

3- Premium between market and official exchange rate

4- Investment to GDP ratio

5- Government expenditure to GDP ratio

6- Liquidity growth rate

7- Nominal rate of rial devaluation

The model also included five dummy variables to control structural breaks and exogenous shocks such as the 1973 oil price boom and the end of the Iran-Iraq war.

The most important finding of the model was the rejection of the hypothesis that the IRR exchange rate converges with its equilibrium values determined by the Purchasing Power Parity model.

The model also found that due to central bank interventions, nominal (market) and real exchange rate had not converged for the past 20 years. However, over the past two years, the CBI’s stabilization policy has narrowed the gap between the nominal (market) and real (equilibrium rate defined by economic fundamentals) exchange rates to less than 20%.

As recommended by many economists, closing this gap is a very important step toward stabilizing the market and signaling economic liberalization.