The Iranian SHAPARAK payment and settlement network processed 814 million transactions in the Iranian month ending December 21, marking a 31% growth year-on-year. The total value of transaction amounted to 810 trillion rials ($26.8 billion), up by 5.28% comparing with the same period in last year.

Currently, 12 authorized Payment Service Providers (PSP) are active in Iran’s e-payment industry with more than 4 million active terminals. SHETAB, the Iranian interbank network with about 30-35 million users, hosts about 200 million transactions every day.

POS terminals also accounted for 78.2% of total electronic transactions in the ninth month of the fiscal year (Nov. 22-Dec. 21), according to the latest data published by SHAPARAK. Internet payment services and mobile payments also accounted for 13.8% and 7.9% of transaction, respectively.

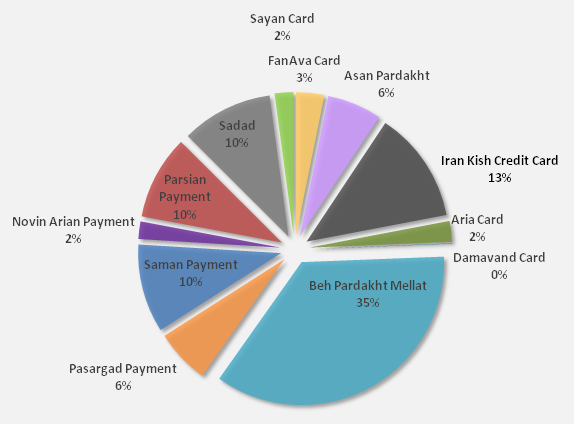

The report also shows that, Beh-Pardakht, a Bank Mellat subsidiary, ranks first among PSPs, accounting for the highest number of transactions, with Asan Pardakht, an independent firm, and Bank Parsian’s E-commerce Company next in line. Beh-Pardakht tops the list in transaction values, followed by Iran Kish Credit Card and Bank Melli’s SADAD.

The majority of PSPs, however, are affiliated to banks with Asan Pardakht the only notable exception. But the company’s earnings ran into trouble after the CBI introduced a ban on mobile payments through Unstructured Supplementary Services Data (USSD), for fear of fraud. The system that uses cell phones for making payments on cell phones was the company’s main business.

Regulatory Bodies

E-banking experts are concerned about the future of the industry and have called for structural reforms including regulatory revision and technological enhancement.

The CBI is in charge of issuing the operation licenses for PSPs and SHAPARAK, which is affiliated to the Informatics Services Corporation, approves their operations technically.

SHAPARAK is still considered a reliable network by domestic users although it has recorded a growth in network errors.

As part of a new plan, the CBI has required PSPs to enhance their structure, security of services, and technology if they want to renew their license.

CBI is also in charge of collecting transaction fees which will be given to PSPs later through SHAPARAK. However, CBI has failed to fully repay its debts to PSPs since April 2014, when the bank owed them a total of 2.71 trillion rials ($90 million).The Money and Credit Council, a policymaking body, even cut PSP subsidies in the same period.

Ineffective Policies

Starting a payment business and obtaining a license is a difficult process due to red tape and high capital adequacy ratio at 400 billion rials ($13.2 million) as of 2014 as well as 1 million rials ($33) for each installed terminal.

Such policies have turned banks into the dominant players in the e-payment industry. At the same time, new businesses’ need for getting rid of the bank’s bureaucratic ways for using their e-payment services, has paved the way for the growth of informal PSPs.

These “payment aggregators”, as SHAPARAK calls them, operate to “help newly established businesses.” They attract more users through simple websites, requiring only an ID card and a bank account.

E-payment providers have improved over the years but visibly lag behind their international peers. Governments across the world try to encourage small businesses and idea developers to market their talent. The CBI needs to do likewise and at the same time promote new businesses and spread public awareness about the new payment systems and their benefits.