The Central Bank of Iran has, for now, put on hold a further cut in the interest rate. The decision, though not unexpected, has led to renewed debates and discussion among economists and businesses on whether or not the CBI should do so.

Proponents of lower rates emphasize on the inverse relationship between interest rates and investment and want early action. Opponents tend to make their case by insisting that under the present economic climate there is simply no need for new rates by decree.

Pro or against, these experts and politicians seem to ignore the reality that we are living in an interrelated economy and economic theory does not always rationalize or determine the causal relationship between variables. Economic theory assumes the sign of correlation between variables, which has been proved to be wrong in some occasions. Above all, economics is not a religion and prominent economists also make huge errors of judgement as they too are humans who try to predict the behaviour of their ilk and fail in the process.

Interest rate is definitely an important determinant of the macro economy and markets can get too hung up on its movements. As such, advocates of cutting interest rates ought to believe that a decrease in rates should be perceived to be so important. Mind you, the previous rate cut did not produce the desired result.

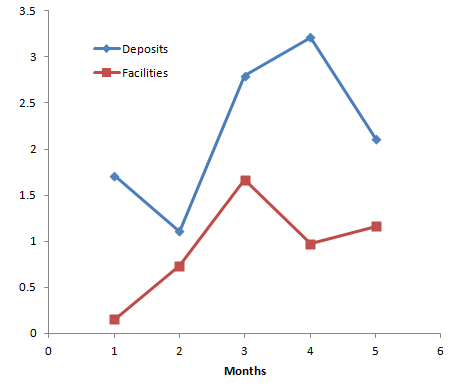

As one would understandably expect, decline in interest rates should be followed by a decrease in savings/deposits and increase in lending and credit facilities. After the 2pp rate cut in April, total deposits in banks shot up a massive 8.3% while the growth rate of credit facilities is less than half that figure (3.8%) according to the CBI data.

This shows that the lending growth rate does not necessarily move in proportion to growth rate of deposits that was expected to be of the descending order. The graph below shows how deposits and credit facilities responded to the rate cut in the second month of the Iranian fiscal year (started March 21). Evidently, the fluctuations in both growth rates of deposits and credit facilities show that other factors are in play, which for all practical purposes, are more important than interest rates, at least in the present Iranian economic state of affairs.

Noticeably, the immediate effect of the rate cut is a steep increase in the growth rate of deposits which is contradictory to what economic theory and logic would suggest. At the same time, though the given credit facilities registered an increase in growth, but barely a month later, that increase took a back seat giving its elevated position to a decrease.

Like many other hot debates, this rather irrelevant and unhelpful debate tends to miss the core issue: the dysfunctional banking system in the country is the elephant in the room. Confluence of bad loans, mismanagement plus the mountain of government debt has questioned the solvency of many banks. It is perceived that there are banks and financial institutions with having more liabilities than their capital.

It seems the government and its economic lieutenants have learnt a lesson from their past experience and this has been commended by champions of the free market who want the government to stay the course and steer clear of any form of intervention. However, this lesson is not very useful in propelling courage and clout needed to reform the bank-dependent economy of Iran. Well, the interest rate is a ‘do or die’ matter for the banking sector and that is why the government has evidently decided to leave the matter to the banks!

Procrastination by successive governments in dealing with the ailing and visibly inefficient banking sector despite repeated warnings and evident symptoms of its failure have made markets, analysts and the general public more anxious about the future.

Businesses are waiting and watching to see how and when the government will go after the underperforming banks, both state-owned and private. By the same token, the common man too is keen to know what the government has in mind for the large number of banks and lending institutions, notably the thousands of unruly and uncertified lenders.

Minus effective government action on these issues of paramount economic importance, most other measures by the Rouhani administration to fix the struggling economy will, at best, be and exercise in futility as they will hardly impress law-abiding Iranians who want a strong government that can succeed and deliver.