The banking industry as a key sector in every economy has undergone enormous evolution in the recent decade. Banks and financial intermediaries are the centerpiece for every economic transaction and that’s why a well-established banking system is essential for economic prosperity.

Therefore, if banks are not in good shape there might be something wrong with the economy. Considering the fact that Iran’s economy is centered on the banking system, here we will look into the current situation to ascertain whether the key industry is plagued by sagging morale.

Prominence of the banking industry in Iran is highlighted in the privatization plan which is in line with the general policies of Article 44 of the Islamic

Republic of Iran Constitution. Following the inauguration of President Hassan Rouhani in 2013, implementation of the aforementioned policies was put high on the government agenda. This eventually led to the financial sector reform in general and the banking industry in particular.

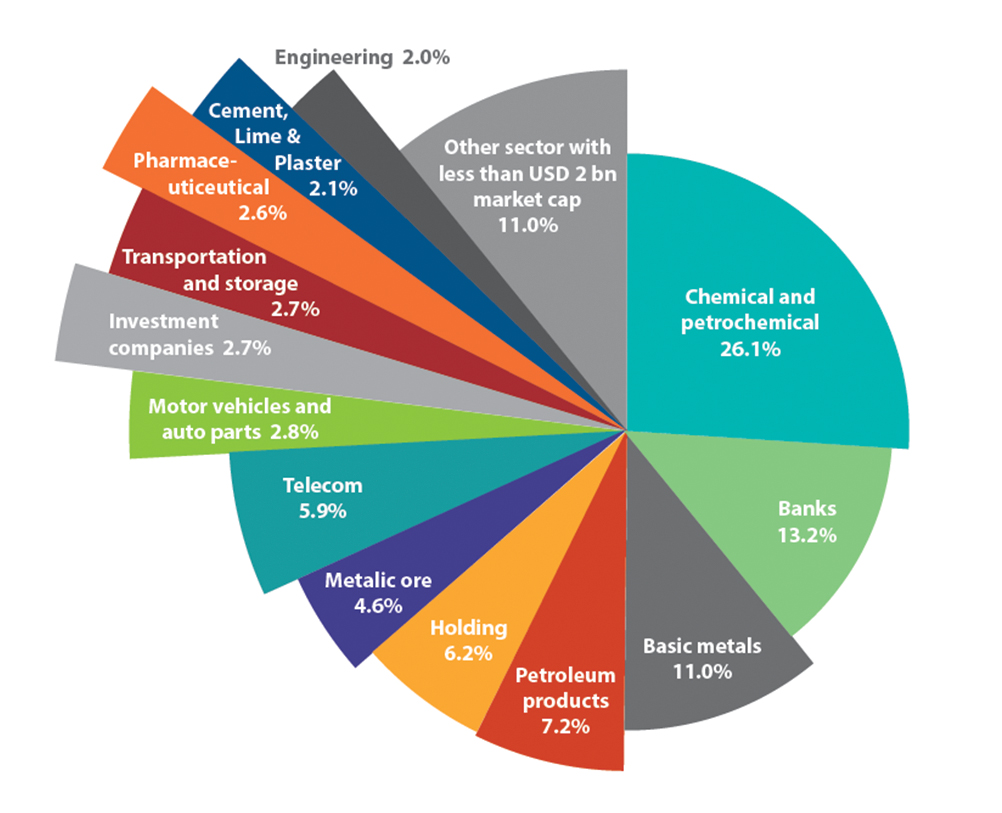

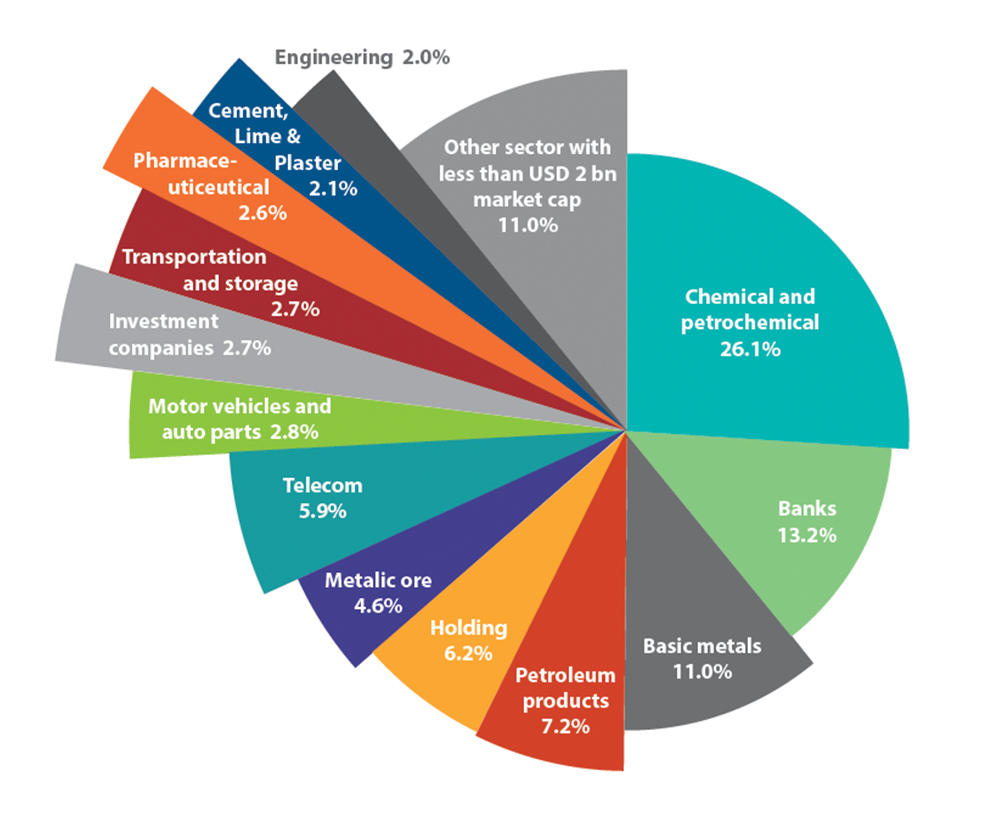

The banking sector constitutes 2.5% of Iran’s GDP. There are currently eight state-owned and twenty private banks as well as four credit institutions of which eighteen are listed on the capital market. The big ones are Bank Sederat, Bank Pasargad and Bank Mellat respectively. With a worth estimated at $11.5 billion, banks represent 13.2% of the capital market.

Due to deficiencies of the equity market, banks are the front-runner to mobilize resources needed for funding businesses looking for capital infusion. Companies in Iran opt for debt financing through the banking sector instead of equity financing or issuing Sukuks through the stock market. In fact the banking sector alone is fulfilling the need for money supply as any failure to bridge the demand gap will have a domino effect in the entire economy.

Lingering Complications

The main problem banks are now facing is intense rivalry to poach savings by offering unreasonably high interest rates. By extension, this has led to higher lending rates and the apparent inability of companies to repay loans. This vicious cycle has caused banks to face long and painful liquidity shortages, the credit crunch and inability to make fresh loans. Add to these the rise in soured loans, especially of state-owned banks.

Another area of concern is that banks are overwhelmed by risky assets. “For now Iran’s banking sector has been applying Basel II standards which stipulate the minimum capital adequacy ratio shall not fall below 8%. Ten out of the 20 listed banks on the stock market are currently below this threshold. So they have little choice but to raise capital which is not a desirable move at the moment”, Mohammad Gorjiara, fund manager at Bourse Behgozin brokerage told the Financial Tribune. The capital adequacy ratio is the percentage of a bank’s capital to its risk-weighted assets.

A persistent problem has been the international sanctions imposed on Iran because of its nuclear energy program that froze part of banks’ overseas assets, disconnecting them from SWIFT - the international interbank messaging network - and deepened the technological gap between the lenders and their foreign peers.

However, with the signing of the nuclear accord with the six world powers this problem is seemingly at least partially resolved. Now the banks can and should prove their worth by being the main conduit for attracting funds from abroad.

Another hurdle is the contractionary and anti-inflationary policies of the government which has made high lending rates unattractive to borrowers. The government finally took the plunge this week by announcing a stimulus package which aims at further quantitative easing by injecting more cash into certain sectors of the economy.

“From a technical point of view a Gartley pattern can be identified in the daily chart of the banking industry which implies there may be a steady 10% growth in the short term. This growth does not seem far-fetched as it is in line with the fundamental prospects for the industry,” Nima Azadi, a market analyst told the Tribune.