A study of non-interest incomes generated by 19 local commercial banks in the past two years has given an insight into the performance of each bank in terms of collecting banking fees and foreign exchange income.

Non-interest income in Iran is primarily derived from fees and foreign exchange lending, Akhbar Bank news websites reported.

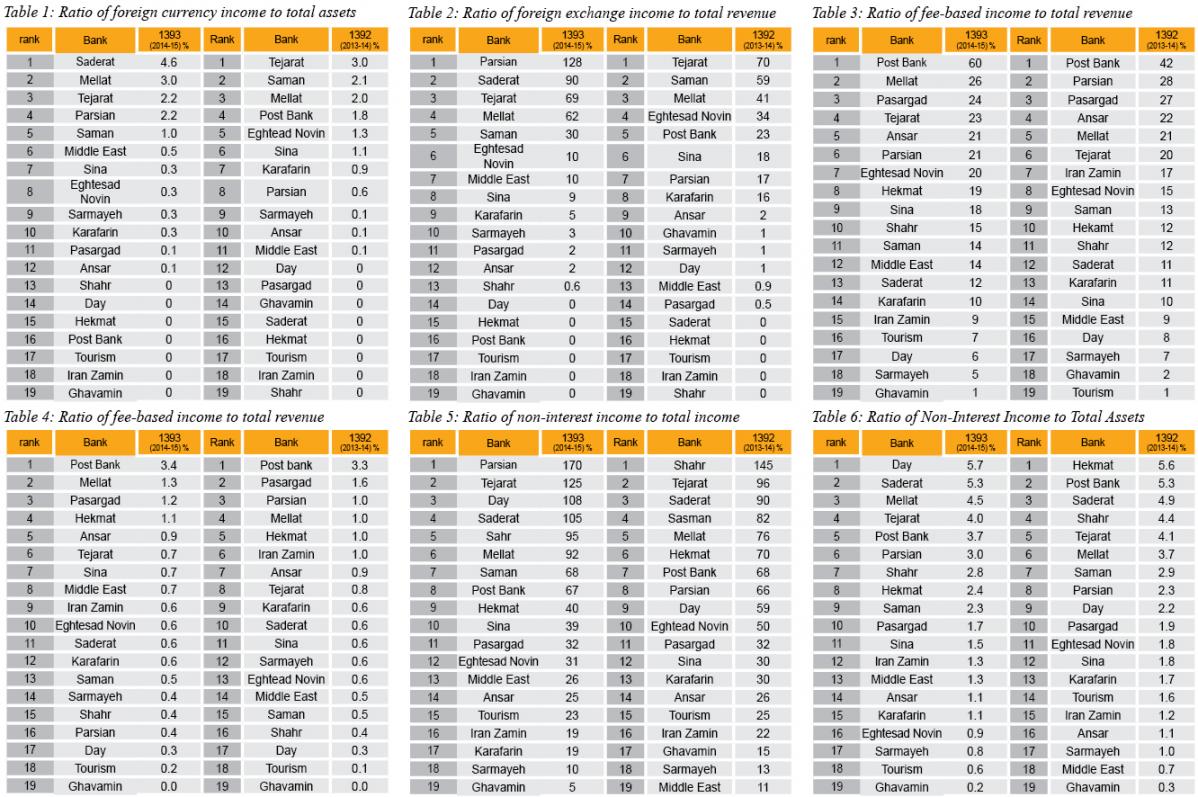

a. Foreign Exchange-Based Income

Whatever the banks receive in foreign currency are categorized under non-interest income. Some Iranian banks open overseas branches to make profit in foreign exchange by either lending or leaving foreign currency deposits in the other Iranian or foreign banks.

Table 1 carries the information on the ratio of foreign exchange income of commercial banks to their assets in 2013 and 2014.

In 2014 Saderat, Tejarat and Mellat commercial banks had more overseas branches compared with other peers, so they had the highest revenue in foreign currency in proportion to their assets. Saman, Eghtesad Novin and Parsian banks also recorded improved performance during the review period. It should be noted that the international sanctions imposed against Saderat Bank dramatically reduced its foreign currency revenues in 2013.

Table 2 shows the ratio of banks’ revenue in foreign currency to their total revenue in 2013 and 2014.

Also in 2014 Saderat, Tejarat and Mellat lenders recorded the best ratios of foreign currency income to total income. Parsian Bank registered lower total revenue in 2014 in light of the decline in its interest income which falsely shows higher foreign currency ratio to total revenue. Tejarat and Saman Banks, in the meantime, recorded better average ratios during the review periods.

b. Fee-Based Income

Fees applied on banking services make up a significant portion of most banks’ revenue. Services such as providing credit cards, issuing guarantee letters, transferring money, granting free-interest loans, and opening letters of credit are among the major sources of fee income.

Table 3 shows the ratio of fee-based income of banks to their total revenue in 2013 and 2014.

Table 4 indicates the ratio of fee-based income of commercial banks to their total assets in 2013 and 2014.

Post Bank was the most successful in terms of generating fee-based income both in 2013 and 2014. Pasargad, Parsian and Mellat respectively followed suit.

c.Total Non-Interest Income

The banks usually include the income generated from selling their assets under non-interest income. To compare the lenders, the ratio of non-interest income to total revenue has been utilized, based on which the ratios for each bank, in 2013 and 2014, are as follows (table 5).

Clearly, Parsian, Tejarat, Day, Saderat in 2014 and Bank Shahr recorded a loss in terms of interest income in 2013. In light of differing strategies adopted by the commercial banks to generate interest income, this ratio is not a suitable indicator to compare the non-interest income of the commercial banks. The ratio of non-interest income of the banks to their assets could, therefore, serve as a better indicator. The following table indicates the ratio for each of the commercial banks in 2013 and 2014:

The table shows that in 2014, among the commercial banks, Day, Saderat, Mellat, Tejarat, Post Bank and Parsian have been more successful in terms of generating non-interest income. Meanwhile, in 2013, Hekmat, Post Bank, Saderat, Shahr, Tejarat and Mellat respectively outperformed other banks in this area.

The comparisons in general suggest that the commercial banks better equipped to generate foreign exchange revenues are more successful in terms of generating non-interest income. In the meantime, the strategies of the banks’ management to encourage clients to use the fee-based services are instrumental to increasing the fee-based income.