Unwinding the sanctions on Iran opens up one of the largest emerging markets to foreign investment and trade. There is huge potential across a range of sectors - in particular oil and gas and various consumer markets. However, there are structural impediments to growth, particularly within the business environment, wrote the Business Monitor Research, a subsidiary of Fitch Group.

Iran presents a huge opportunity to investors across almost all sectors, and the outlook for the country’s economy over the next decade is bullish as sanctions are removed from 2016. In broad terms, Iran is the 29th largest economy globally, its population is relatively well educated, and its large consumer base and relative wealth offers enormous opportunities to the auto, ICT and food and drink industries, among others.

However, the nuclear deal will not remove the enormous structural problems in doing business in Iran, and this will temper the growth outlook.

Given the huge amount of investment needed, an immediate boom in Iran’s economy following the relaxation in sanctions is unlikely. However, pent-up demand, positive demographics, a skilled workforce, and a large hydrocarbon and consumer story all make Iran perhaps the most positive and relatively well-balanced growth story in the Middle East over the next decade.

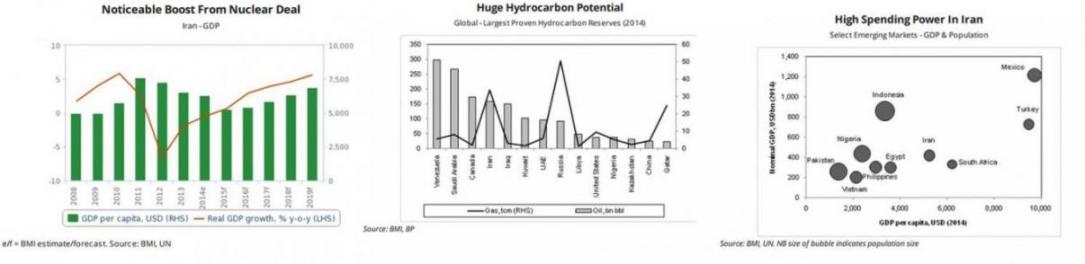

Iran’s oil and gas sector presents one of the most exciting opportunities globally. Iran has the fourth largest oil reserves and second largest gas reserves globally, and years of sanctions have kept the industry far below potential. While Iran will certainly not allow unfettered access to its oil reserves given historical suspicion and its desire to protect industries of national security, the government is likely to push for partnership with local firms. Even with these restrictions, as well as substantial investment deficits, the country has enormous potential. BMI’s Oil & Gas team expects Iran’s oil production to reach 4.1 million b/d in 2020, an additional 640,000 b/d from current levels - the largest increase in the Middle East over the period.

While Iran’s oil reserves have received the lion’s share of media interest of late, the country has huge potential as a consumer market, which accounts for 44% of GDP - one of the highest shares in the region. As well as having a population of 80 million (the second highest in the Middle East after Egypt), Iran’s GDP per capita compares favorably with similar emerging markets (see chart).

This potential as a consumer market is well illustrated in the auto sector. BMI’s auto team forecasts vehicle sales and production to grow by 13% and 14% respectively per annum over the next five years - the fourth highest rate globally. Peugeot is expected to regain its previous position of dominance, but the arrival of new brands will give consumers the choice they have been lacking in recent years.

Similarly, BMI forecasts an uptick in foreign investment in the food and drink sector from 2016, thanks to lower insurance and transport costs, the reintegration of Iran into the international banking system and the attractiveness of Iran’s largely untapped consumer base.

On the business environment front, there are a few positives awaiting investors into Iran. The country has a relatively skilled workforce by regional standards, with 98% of labor force possessing formal education and a tertiary enrolment ratio of 55.2%, the third highest in the Middle East and North Africa. Furthermore, the improving investment climate in Iran could tempt skilled workers who have emigrated over the past years to return to the country.

However, issues including poor rule of law and absence of intellectual property rights will remain a persistent concern for investors. Entrenched risks are present in all four sections of BMI’s Operational Risk Index, for which Iran is behind both the Middle East and North Africa average and emerging market peers.

Iran’s score of 34.4 out of 100 for Trade and Investment Risk places it 14th out of 19 states in the Middle East and North Africa region. With an easing of sanctions, Iran’s Trade and Investment Risk score will rise to 40.6 out of 100 over the medium term, but it is still behind countries of similar economic size and population.

These structural challenges are further illustrated in the ICT sector. Indeed, the high cost of doing business is illustrated by the taxes imposed on ICT products; these taxes are by far the highest in the region. In an attempt to protect the domestic industry, as well as to reap the benefits of better trade relations, BMI expects the government will keep import tariffs on consumer electronics and other goods high. Therefore, while the group expects the relaxation of sanctions to reduce costs and improve purchasing power to a certain extent, high taxes and other operational risks will prevent many players in the technology sector from rapidly moving to exploit the market’s potential.