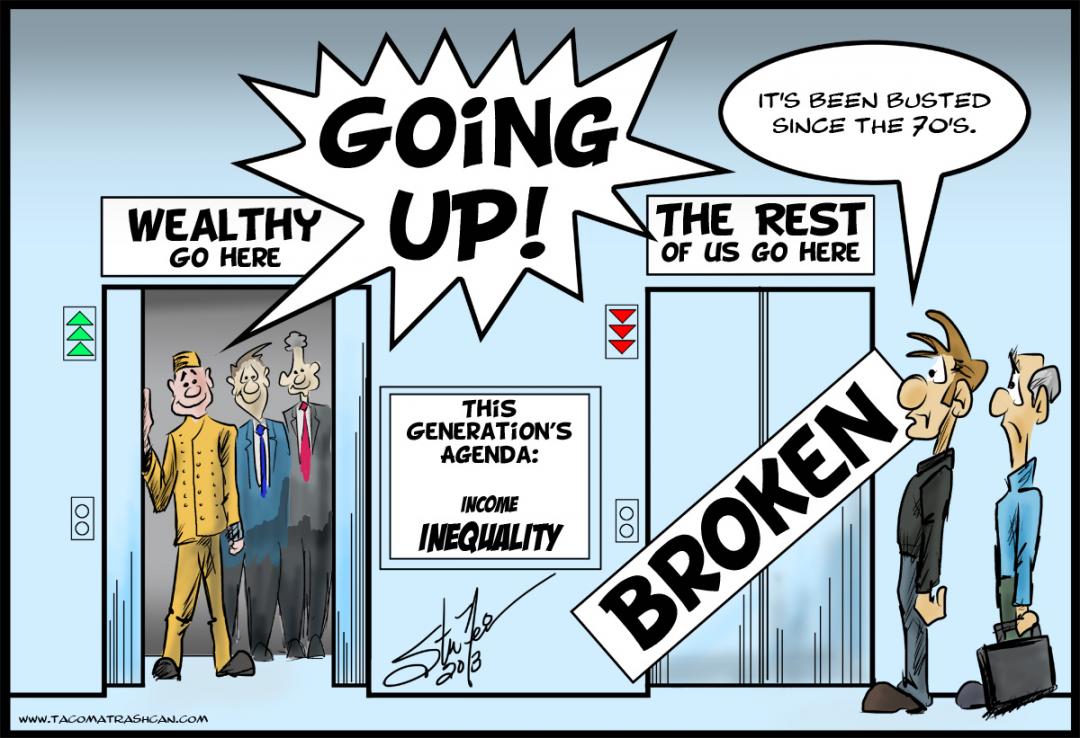

The issue of rising income inequality loomed large at this year’s World Economic Forum in Davos. As is well known, the United States’ economy has grown significantly over the past three decades, but the median family’s income has not. The top 1% (indeed, the top .01%) have captured most of the gains, something that societies are unlikely to tolerate for long.

Many fear that this is a global phenomenon with similar causes everywhere, a key claim in Thomas Piketty’s celebrated book Capital in Twenty-First Century. But this proposition may be dangerously misleading, Ricardo Hausmann said in his opinion column in Project Syndicate.

It is crucial to distinguish inequality in productivity among firms from unequal distribution of income within firms. The traditional battle between labor and capital has been about the latter, with workers and owners fighting over their share of the pie. But there is surprisingly deep inequality in firms’ productivity, which means that the size of the pie varies radically.

This is especially true in developing countries, where it is common to find differences in productivity of a factor of ten at the provincial or state level and many times higher at the municipal level.

These two very different sources of inequality are often conflated, which prevents clear thinking on either one. Both are related to a similar feature of modern production: the fact that it requires many complementary inputs. This includes not only raw materials and machines, which can be shipped around, but also many specialized labor skills, infrastructure, and rules, which cannot be moved easily and hence need to be spatially collocated. A shortage of any of these inputs can have disastrous effects on productivity.

Key Inputs Missing

This complementarity makes many parts of the developing world unsuitable for modern production, because key inputs are missing. Even within cities, poor areas are so disconnected and inadequately endowed that productivity is dismal. As a result, there are huge disparities among firms in terms of efficiency – and hence in the income they can distribute.

Given productivity constraints, redistribution is only palliative, not curative. To address the problem requires investing in inclusion, endowing people with skills, and connecting them to the inputs and networks that can make them productive.

The dilemma is that poor countries lack the means to connect all places to all inputs. They are faced with the choice of connecting a few places to most inputs and getting high productivity there, or putting some of the inputs in all places and getting very little productivity growth everywhere. That is why development tends to be unequal.

Distribution

The other problem of modern production is how to distribute the income generated by all of the complementary inputs. Today, production is carried out not just by individuals, or even by teams of people within firms, but also by teams of firms, or value chains.

Economists have traditionally believed that each team member is paid her opportunity cost, that is, the highest income she could receive if she were kicked off the team. In this context, if markets are characterized by what economists call perfect competition, once the opportunity cost of all inputs has been paid, there is nothing left to distribute.

Team Surplus

Who gets to pocket this “team surplus”? Traditionally, the assumption has been that it accrues to shareholders. But the rise of extreme CEO compensation in the US, documented by Piketty and others, may reflect CEOs’ ability to disrupt the team if they do not get part of the surplus. After all, CEOs experience precipitous income declines when they are kicked out, indicating that they were paid far more than their opportunity cost.

In the case of successful start-ups, the money paid when they are acquired or go public, accrues to those who put the team together. For more conventional value chains, the surplus tends to go to the inputs that have greater market power.