The number of people registering as insolvent in England and Wales hit a five-year high in the third quarter, according to figures on Friday that hinted at trouble brewing in Britain’s consumer economy.

The government’s Insolvency Service said 27,807 people in England and Wales registered as insolvent between July and September, up from 22,389 in the three months to June and marking the biggest total since the third quarter of 2012. On a seasonally adjusted basis, the figure was just short of a three-year high struck in the first quarter of 2017, news outlets reported.

Personal insolvencies rose by 11% in the three months to September, figures from the Insolvency Service have shown. Personal insolvencies have been rising over the past couple of years, largely due to changes in regulation that have made debt relief for consumers easier to obtain, according to experts in the field.

But debt charities and the Institute of Chartered Accounts in England and Wales warned that the latest sharp increase indicated wider problems in Britain’s consumer-led economy.

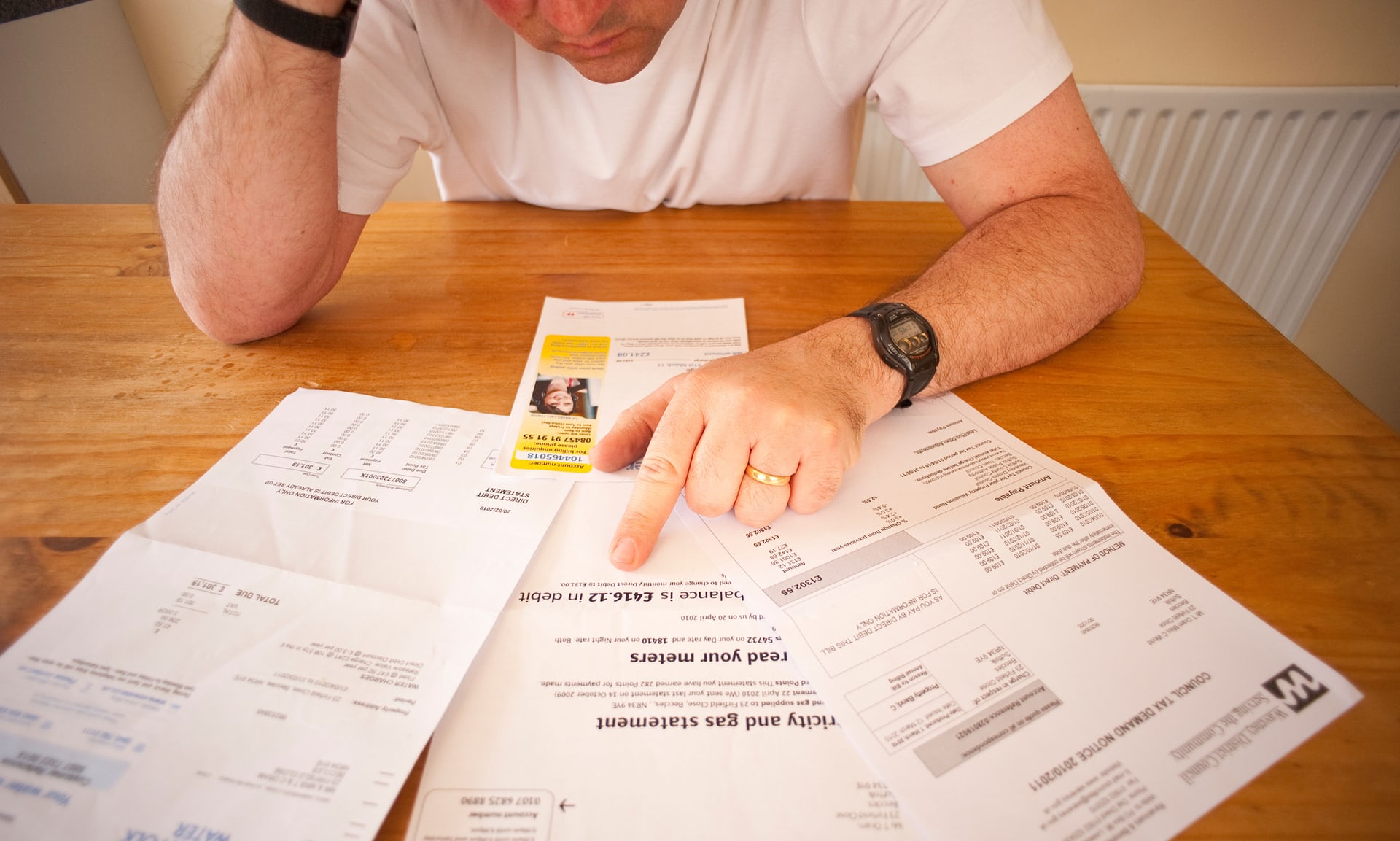

Household budgets have been strained by rising prices caused by the pound’s drop after last year’s Brexit vote, and wage growth has failed to keep pace.

The insolvency figures are likely to bolster the view of economists who worry that even a small rise in Bank of England interest rates could have an outsized impact on consumers.

A clear majority of economists in a Reuters poll published on Tuesday expect the BoE will raise interest rates next Thursday to 0.5% from 0.25%—although most also said it would be a mistake to act now.

“With household debt levels continuing to rise, we are concerned that more families will be pushed into difficulty if circumstances change,” said Jane Tully, director of external affairs at the Money Advice Trust charity, Reuters said.

The figures showed the increase in personal insolvency was down to a rise in individual voluntary arrangements—a debt relief measure short of bankruptcy.

Businesses Could Suffer

The ICAEW said the insolvency figures boded poorly for the wider economy. “Consumer insolvencies are a reliable marker of business challenges ahead,” said Clive Lewis, head of enterprise at the ICAEW.

“We anticipate a worsening scene for businesses in the forthcoming quarter and would urge all owner-managers to look out for early signs of trouble and act fast to address them.” Lewis said he thought even a small increase in interest rates could persuade consumers that they were not able to afford contracts that they had entered into, citing loans for car purchase as a particular area of concern.

Businesses should also be deeply concerned about the substantial increases in personal insolvencies, according to Bob Pinder, regional director at the ICAEW, adding that he was concerned that businesses might be lulled into a false sense of security by low corporate insolvency rates.

“Consumer insolvencies increasing at this rate will almost certainly trigger considerable business risk and they must be able to identify the early warning signs fast, and take immediate actions to ensure they are not the ones to become next quarter's statistics," he explained.

The BoE has said there is no overall debt bubble in Britain but it has expressed concern about consumer debt, which had been growing at about 10% a year.

Insolvencies Rising Since 2015

There were 6,274 debt relief orders—a write-off alternative to bankruptcy if an individual owes less than £20,000—and 3,682 bankruptcies.

Adrian Hyde, president of R3, the UK’s insolvency and restructuring trade body, said that these figures were the result of “falling real wages and exhausted credit limits”. Apart from the odd quarterly dip, he noted, the overall trend of insolvencies has been rising since the second half of 2015.

“Some people have trouble paying for basics, like food or housing, let alone paying for luxuries. R3’s long-running survey of personal debt levels typically finds around two-in-five people saying they often or sometimes struggle to make it to payday,” Hyde said.

Alec Pillmoor, a personal insolvency partner at tax consultancy firm RSM, believes that these statistics may signal increasing numbers of financially troubled households in 2018, particularly as those who had resorted to credit, face an interest rate rise, following the imminent rates decision from the BoE.

"Should the widely predicted increase in interest rates occur next week, this will have a significant effect on those households that are just managing on their income,” he said.